Nitrogen+Syngas 364 Mar-Apr 2020

31 March 2020

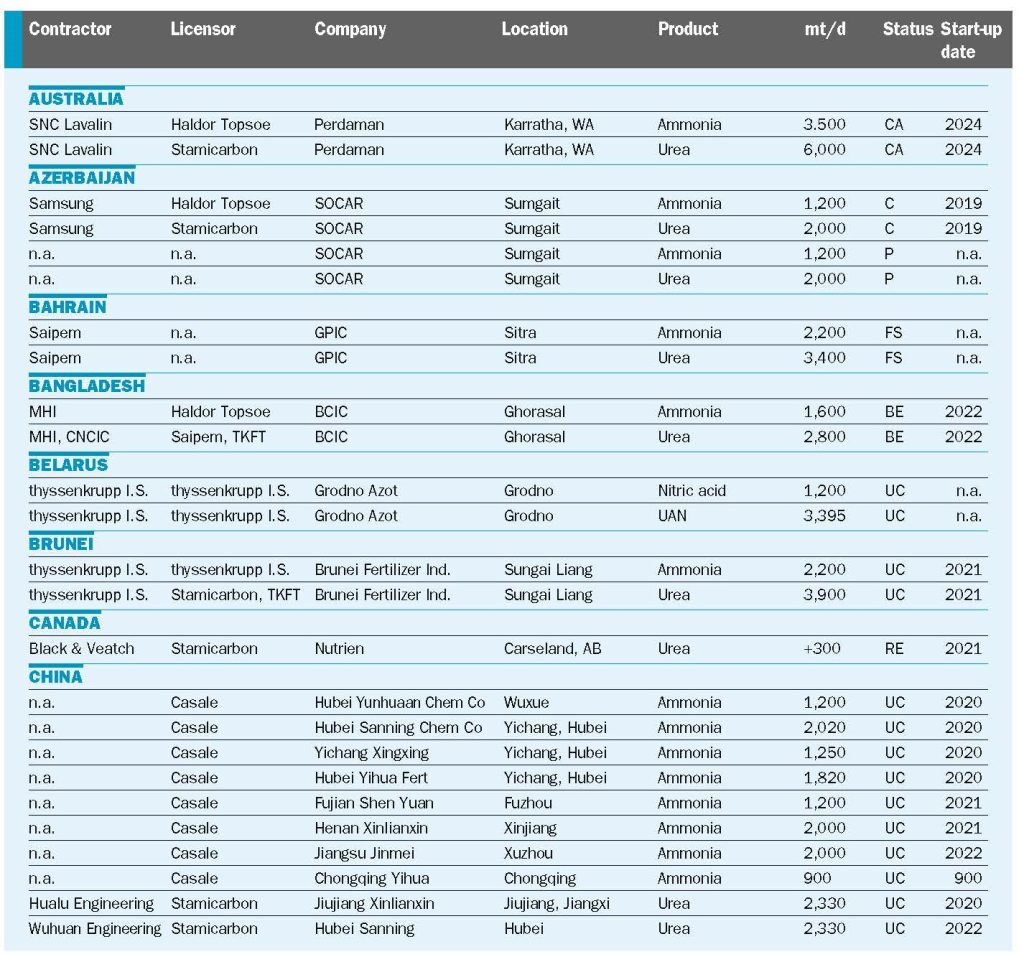

Nitrogen Project Listing 2020

Nitrogen+Syngas’s annual listing of new ammonia, urea, nitric acid and ammonium nitrate plants shows that the key areas for new project developments are Egypt, India, Nigeria and Russia. The timing of new Iranian capacity remains subject to external sanctions, while other significant projects are under way in China, Brunei and Uzbekistan, and the new ammonia plant for Ma’aden in Ras Al Khair to produce diammonium phosphate. Currently however the number of new projects scheduled for beyond 2021 is relatively small, although a number of the current batch of projects are likely to slip.