Sulphur 398 Jan-Feb 2022

31 January 2022

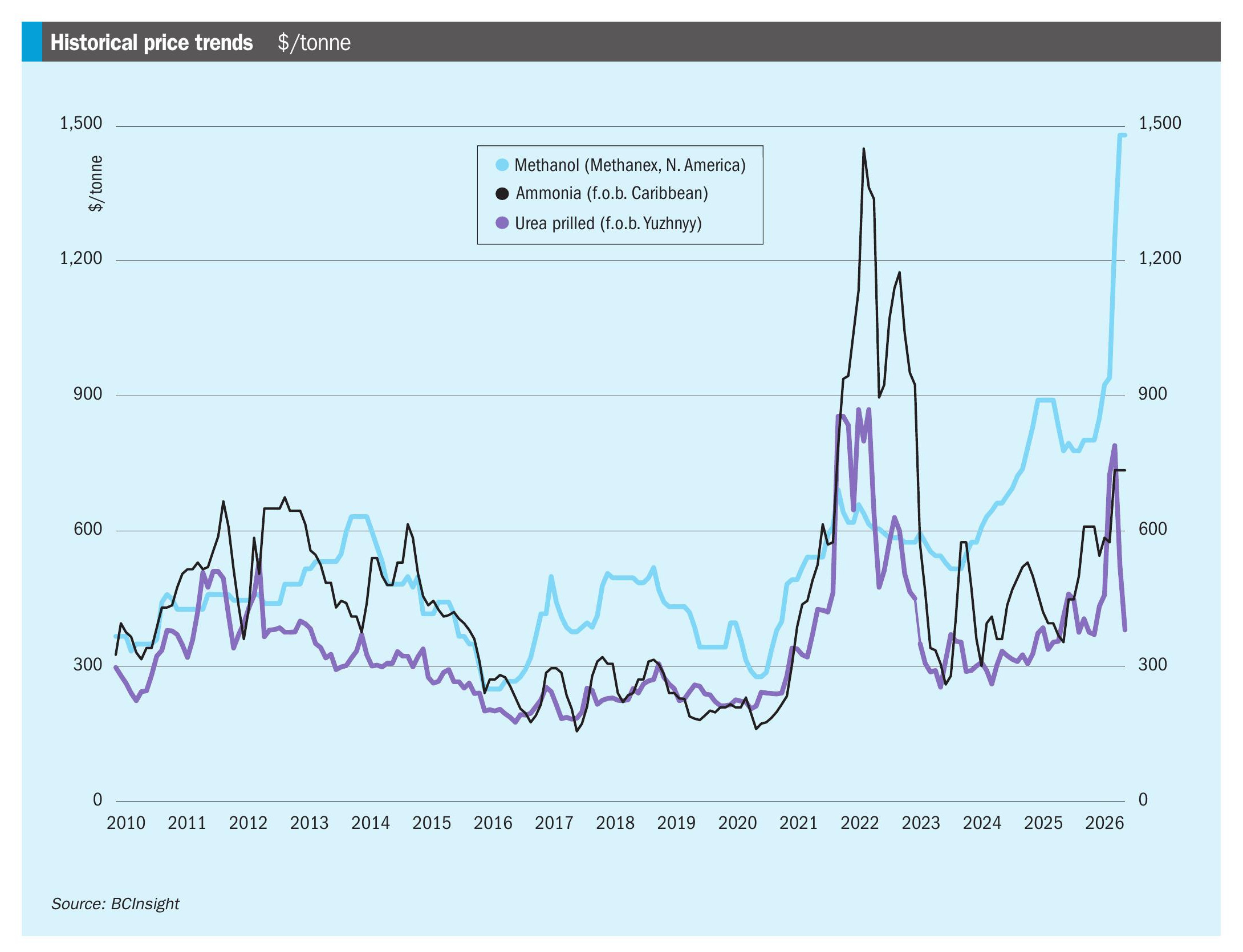

A co-product again

“There are signs that this particular sulphur price spike may be fairly short-lived”

It’s a slightly dispiriting fact about the sulphur industry that most of its producers don’t really want it. If you’re a refiner or a sour gas producer, you mainly care about the diesel and gasoline or natural gas that you can process and sell, and the sulphur is just the inconvenient component that the law and your customers force you to remove. But at times when sulphur prices, as they have at the start of this January, reach levels as high as $300/t, then the industry standing joke is that sulphur suddenly stops being a by-product or waste product, and starts to become a ‘co-product’ instead.

The last time that sulphur prices reached this level was the 2008-09 price spike, a time when China’s rapid industrialisation and consequent overheated commodity markets, coupled with overheated financial markets that eventually led to the great crash, drove sulphur spot rates to briefly reach unheard-of levels of $800/t. As former ASRL head and long-time industry commentator Jim Hyne said to me at the time: “somebody out there is making a lot of money”, though it was often hard to get anyone to admit to who that might be. Even so, the current price spike is a remarkable turnaround considering that at the start of 2020, sulphur prices were down at $40/t f.o.b. Middle East.

This time of year is often a tighter time for sulphur markets, with availability from Central Asia constrained by weather. But on top of that, phosphate markets have been heading skywards as China cuts back on exports and the US imposes tariffs on product from Morocco and Russia. Russian fertilizer export quotas have merely exacerbated an already tight supply situation. Sulphuric acid markets are also tight, with European smelter acid production down due to maintenance turnarounds and nickel demand for battery production rising rapidly, boosting the need for sulphur-burnt acid.

There are signs that this particular sulphur price spike may be fairly short-lived; perhaps only a couple more months, and we needn’t start melting down the Canadian stockpiles just yet. More sulphur is starting to flow from completed refinery projects in Kuwait and Saudi Arabia, and we should soon see, at long last, the impact of the much-delayed Barzan LNG project in Qatar. The gradual addition of 3 million t/a of sulphur capacity between the various projects should be enough to calm markets and bring prices back down by the end of the year. For now, though, the sulphur industry can enjoy another brief period of being a co-product again.