Nitrogen+Syngas 377 May-Jun 2022

31 July 2022

Turning points

“The impact of high fertilizer prices on global food production remains a serious concern”

On February 27th, in a speech to the Bundestag, Germany’s chancellor Olaf Scholz described the events then unfolding as a “zeitenwende” – a historical turning point. He was speaking of German foreign and security policy, but it seems likely that Russia’s February 24th invasion of Ukraine may end up marking a break with the past in many different ways. Last issue’s Editorial was written when Russia’s ‘special military operation’ was still only a few days old, and the situation was still very fluid. Two months on, and for all of the uncertainties remaining, some glimpses of the way that things are changing are becoming clearer.

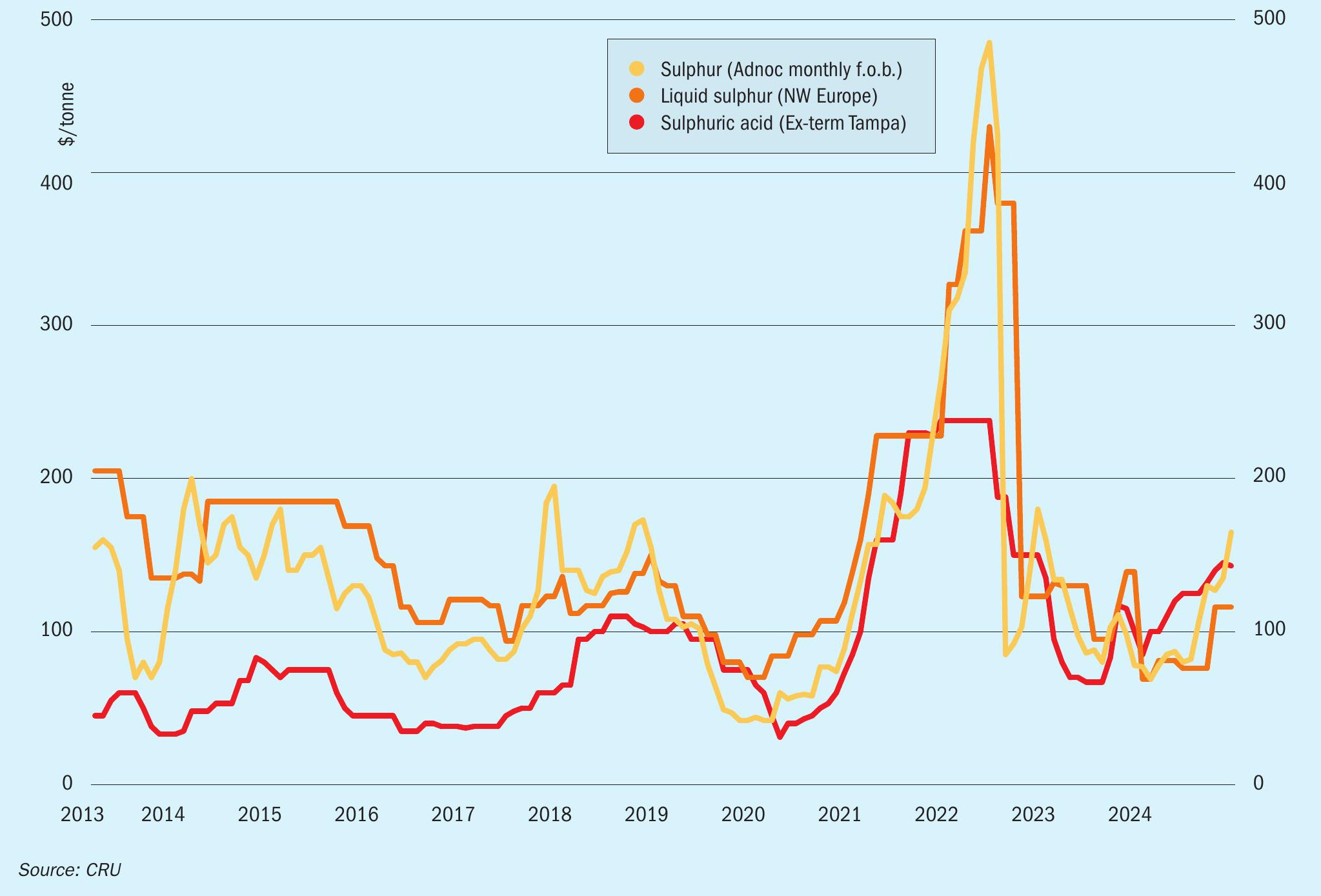

The effect on ammonia markets has been as serious as feared, as the price graphs on page 7 bear out. Unheard-of price levels of $1,650 per tonne have been recorded in Tampa, and US agricultural economists have talked seriously about prices reaching $2,000/t. The impact on urea has not been quite as dramatic, after an initial price spike, but phosphates and potash markets have also seen record price levels, and the impact of high fertilizer prices on global food production remains a serious concern. Former IFA Director General Charlotte Hebdebrand, working now for the International Food Policy Research Institute, charted the potential impact upon developing countries in a recent blog post. Noting that some countries such as India and China may be able to buffer the price shock via subsidy regimes, she adds: “but those regimes are going to place tremendous fiscal pressure on budgets already stressed by substantial government outlays during the covid-19 epidemic. Relatively smaller markets, especially many African countries, face a particularly difficult situation, as producers and traders are likely to favour shipping limited supplies to larger markets. Given Africa’s still-limited use of fertilizers… a decline in fertilizer use would lead to significantly reduced productivity for the continent, with potentially serious consequences for food security.”

The impact on energy markets has been equally serious, muted slightly by the new covid lockdowns in China, but base prices for oil look set to hover around $100/bbl for most of the rest of the year, according to the most recent forecast by the US Energy Information Administration, and Henry Hub gas prices are predicted to stay at $7.00-8.00/ MMBtu for the remainder of 2022. This latter is not so serious for the US, which has been insulated by its gas surplus from the worst effects of a loss of Russian supply. However, in Europe the situation is very different. Europe was in a gas price crisis even before the events of February, and even with gas still flowing from Russia to Europe through Ukraine’s pipelines – too important a trade for either side to be willing to end it for now – European wholesale gas prices have stabilised at $35.00/MMBtu. But at time of writing Russia has stopped deliveries to Bulgaria and Poland, and Ukraine had just announced it would be closing some stretches of the pipelines which carry one third of the gas across its territory. There has been a knock-on effect on global LNG prices, which were around $25.00/MMBtu in Asia at the start of May.

If there is a silver lining in any of this gloom, it may be that it rapidly accelerates a transition towards the use of renewable energy, including in ammonia and methanol production. A recent Bloomburg publication assesses the price for producing ammonia using water electrolysis to generate hydrogen at around $500-700/t at present; expensive in the context of 2020 price levels of $200/t, but looking like quite a bargain in the current market. Europe and India have both struggled with providing affordable feedstock for domestic nitrogen fertilizer production – could renewables offer them a way out of this dilemma? That could be a turning point indeed.