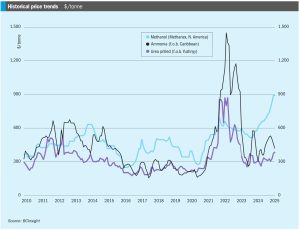

Global sulphur benchmarks rallied at the end of February, underpinned by strong demand in Indonesia and stock drawdowns in China as fresh European sanctions on Russia targeted the port of Ust-Luga. Chinese buyers paid up to $225t/t c.fr for a cargo, with unconfirmed rumours of business at even higher levels. However, delivered prices still lag domestic port spot prices in China, which are now assessed at a delivered-price equivalent of around $242/t c.fr. China’s delivered sulphur price jumped significantly as port inventories declined, and new arrivals were limited. Only two new cargoes were reported in the last week of February, one from a mainstream source into southern China at $205/t c.fr, and the second at $225/t c.fr by a phosphate producer for the Yangtze River. The sulphur port spot transaction price is reported at around 2,0402,050 yuan/t FCA ($281-283/t), with the low-end up $26/t and high-end up $25/t compared with previous settlements. That port price indicates delivered values at around $242/t c.fr, which is $17/t higher than the import price on the Yangtze. Phosphate producers need to purchase more sulphur to meet the increased buying activity in northeastern market and the improving spring application season demand in northern China. Still, market sales availability is limited, as most port tonnes are held by traders instead of end-users, while traders are selling limited quantities now to push prices higher. Chinese total port inventory dropped to 1.89 million tonnes by 26 February 2025. The quantity at Yangtze river ports declined 59,000 tonnes to 633,000 tonnes, while Dafeng port inventory decreased 20,000 tonnes to 450,000 tonnes.