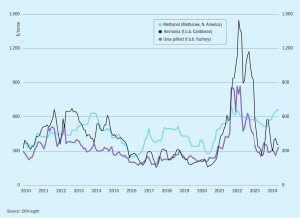

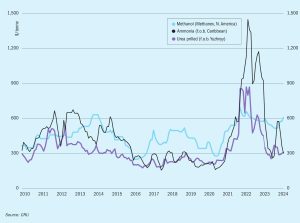

A sea change?

In our May/June issue I discussed the race to be the next major green shipping fuel, in which methanol and ammonia both remain significant contenders, but which methanol appeared to be pulling ahead in. But more recently, a few stories from the past few weeks have left me not quite as sure as I was about that. Firstly, there’s the news in our Syngas News section this issue that the FlagshipONE green methanol project in Sweden is being delayed and possibly abandoned, because demand for green methanol for shipping has not actually materialised as fast as was anticipated.