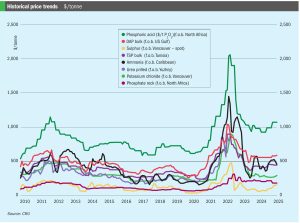

Sulphur prices soaring

The past few weeks have seen sulphur prices spiking after a steady rise since 3Q 2024. At time of writing, delivered prices to a variety of locations were around $280/t c.fr, their highest level since mid-2022 when the price of commodities of all kinds jumped in the wake of the Russian invasion of Ukraine and subsequent sanctions. Steady buying from Indonesia and China, the two largest importers of sulphur, appears to have supported the market, in China’s case mainly for phosphate production as well as a variety of industrial processes, and in Indonesia’s case to feed the high pressure acid leach (HPAL) plants that are producing nickel for the battery and stainless steel industries. Although Chinese buying has dropped off slightly since Lunar New Year, and demand has also slackened in India, Indonesia’s appetite continues unabated, having tripled its nickel production since the start of the decade to become the world’s largest producer, representing 60% of global supply in 2024.