A broken system with affordability and availability challenges

Peter Harrisson , Principal, Sulphur & Sulphuric Acid Market Services, provides an overview of the global sulphur market.

Peter Harrisson , Principal, Sulphur & Sulphuric Acid Market Services, provides an overview of the global sulphur market.

We speak to Justin Rackleff, CRU’s Americas Lead, Fertilizer Value Chain, about the US market state-of-play ahead of this year's Southwestern Fertilizer Conference.

We interview Alison Coughlin, CME Group’s Director of Commodity Research and Product Development, about the valuable market role of fertilizer futures.

The U.S. Department of Agriculture (USDA) has launched the $500 million Fertilizer Investment & Expansion for Long-Term Domestic Supply (FIELDS) Programme to expand domestic fertilizer manufacturing and reinforce the U.S. fertilizer supply chain.

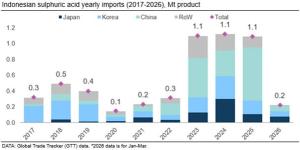

As Indonesia's nickel industry drives significant import demand of sulphuric acid in recent years, CRU is launching a new weekly CFR Indonesia acid price assessment on 28 May to bring transparency to this key spot market.

Canada’s new National Food Security Strategy makes fertilizer access, approvals and supply security a core part of federal efforts to lower food costs and cut exposure to global shocks.

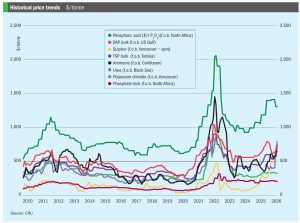

Price trends and market outlook, 7th May 2026.

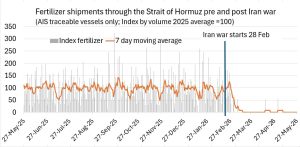

Strait of Hormuz disruptions linked to the Iran war have choked off fertilizer shipments from the Middle East and pushed prices sharply higher, prompting a wave of emergency support and trade measures as governments try to shield farmers ahead of key planting seasons.

China’s sulphuric acid exports fell 49% year on year to 666,808 t in the first four months of 2026 as Beijing moved from quota controls to a full export halt from May, removing a key supplier from the seaborne market at a time of already tight balances.

Brussels has put Europe’s gas‑exposed fertilizer industry at the centre of its new Fertilizer Action Plan, warning that high energy costs and plant closures threaten the region’s nitrogen capacity and long‑term food security.