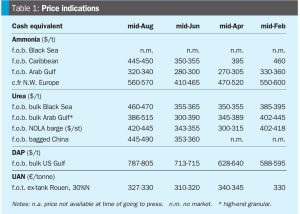

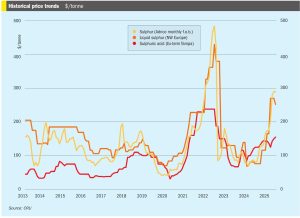

Market Outlook

• The global sulphur market is forecast to enter a downward trend as supply from Saudi Arabia normalises following the summer months, while demand decreases alongside demand for phosphate fertilizers. The price is expected to fall towards the end of the year, with a low of around $220/t by May 2026.