Market Outlook

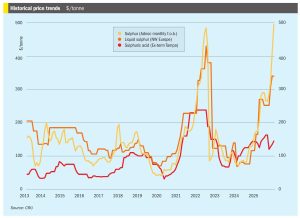

• CRU’s latest global sulphur forecast is for a January price peak before a decline, with the key downside risk being a sharper correction if the supply deficit closes faster than expected. The global sulphur market’s upward momentum has been slowing, with attention shifting to geopolitical risks in Iran. Despite limited physical disruption being reported, the upside risk to prices could be substantial. Following the US bombing of an Iranian nuclear facility back in June, supply from Iran became bottlenecked, despite good production levels, as vessel owners became unwilling to call at ports like Bandar Abbas due to the increased risk.