How to solve stripper efficiency issues (part 5)

In part 5 of this series on stripper efficiency issues we conclude the discussion with a focus on fouling inside stripper tubes.

In part 5 of this series on stripper efficiency issues we conclude the discussion with a focus on fouling inside stripper tubes.

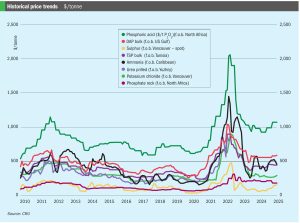

Price trends and market outlook, 20th February 2025

Hulunbeier New Gold Chemical Co has selected Stamicarbon to revamp a urea plant in Hulunbuir, northeastern Inner Mongolia.

Days 2 and 3 of the CRU’s 38th Nitrogen+Syngas 2025 Expoconference turned to the technical sessions, organised in three parallel streams covering: green ammonia technology, nitric acid and ammonium nitrate, plant operations and reliability, urea technology, digitalisation, carbon capture, emissions reduction and sustainable fertilizer production, and fertilizer finishing.

CRU recently relaunched its Fertilizer International and BCInsight Platform. This relaunch coincided with the Fertilizer Latino Americano (FLA) conference in Rio de Janeiro, where we issued our inaugural sentiment survey for delegates. This insight presents and analyses the survey results, which point towards an optimistic tone for 2025 markets in Brazil and beyond. Prices are […]

Ammonia markets saw a slow start to 2025, with further transparency needed on both sides of the Suez to determine the extent to which prices are expected to fall through January amid healthy supply and only limited pockets of demand.

Prices in most markets should register declines through January, though the extent to which benchmarks will ease is yet unclear. Chinese suppliers have seen significant price declines in recent weeks.

In Part 4 of this series on stripper efficiency issues, we continue to look at the causes of lower stripper efficiency with a discussion on the high delta-P range of liquid dividers.

Carbon Recycling International (CRI), which operates a geothermally powered green methanol plant at Svartsengi, 40km southwest of Reykjavik, had to evacuate its site in late November when a 3km fissure opened in the earth a few kilometres away and lava began spilling across adjacent land. Satellite photos of the area taken on November 24 show a large field of molten and cooled lava to the north, west, and south of Svartsengi, though the plant itself remained undamaged. CRI’s Iceland facility runs on CO2 , water, and renewable electricity from the Svartsengi geothermal power station. CRI says the low-carbon energy source allows it to produce 4,000 t/a of methanol with a greenhouse gas footprint just 10–20% that of conventional methanol.

A complete list of all articles and news items appearing in Nitrogen+Syngas magazine during 2024.