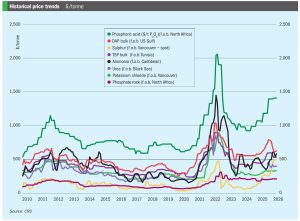

Middle East conflict drives historic urea affordability crisis

An update on the impacts of the Middle East conflict on fertilizer markets.

An update on the impacts of the Middle East conflict on fertilizer markets.

Price trends and market outlook, 26th February 2026. (Important note: this Market Insight was published two days before the start of the latest Middle East conflict.)

Diaphragm seals are applied when pressure or level transmitters need to be protected against harsh conditions like the corrosive ammonium carbamate in urea plants. The process pressure is transmitted via the flexible diaphragm and transmission fluid to the measuring instrument as shown in Fig. 1 below.

The government of Pakistan has published a ‘strategic roadmap’ for the country’s major Coal-to-Fertiliser (C2F) initiative. The project is being executed by the publicly-owned Fauji Fertiliser Company (FFC), and will use local coal reserves at Thar as feedstock for the ammonia plant, which will in turn feed 720,000 t/a of urea capacity. The $1.1 billion project aims to strengthen the country’s fertiliser security as well as add value to local resources. A bankable feasibility study was completed in November 2025, and the project is now in the Front-End Engineering Design (FEED) and project agreements phase. Under the proposed timeline, financial closure is expected between late 2026 and 2027, while commercial operations are targeted to commence in January 2031.

Changing markets for feedstock, shifts in demand, carbon pricing and geopolitics all help dictate the location of new urea capacity.

Polymer manufacturer Covestro has signed a memorandum of understanding with ammonia and urea exporter Fertiglobe and chemical producer TA’ZIZ to explore collaboration across the ammonia and nitric acid value chains. The MoU reflects the parties’ shared interest in assessing both near-term supply solutions and longer-term opportunities supporting the transition toward lower-carbon production pathways. The agreement was signed during the visit of German Chancellor Friedrich Merz to the UAE.

Nitrogen+Syngas ’s annual listing of new ammonia, urea, nitric acid and ammonium nitrate plants.

Madras Fertilizers Limited (MFL) has submitted a proposal for a new $1.1 billion greenfield ammonia-urea manufacturing project in Chennai, aimed at strengthening domestic fertiliser production and reducing import dependence. The company says that the project is aligned with the government’s broader push for self-reliance in critical agri-inputs and improved food security. The proposed plant will have a capacity of 1.3 million t/a of urea and is currently at the feasibility study stage, but MFL says that its existing 1970s vintage plant is already running at 120% of nameplate capacity, and that a new larger scale facility would see significant improvements in output and operating efficiency.

• Prices are likely to remain on an upward trajectory as long as the Strait of Hormuz remains effectively closed and Middle East export availability is constrained.

In just its first two months, 2026 had already managed to be a rollercoaster of a year, but at the start of March, the onset of hostilities against Iran by the US and Israel has managed to deliver another huge shock to markets, particularly commodities. Iran’s strategy of widening the conflict to neighbouring states, including by attacking Qatar’s massive LNG facility at Ras Laffan, effectively shutting it down, has sent the LNG market into chaos, and attacks on several tankers and other ships have paralysed maritime insurance markets and by default achieved the long-feared closure of the Straits of Hormuz.