People

A summary of recent company appointments.

A summary of recent company appointments.

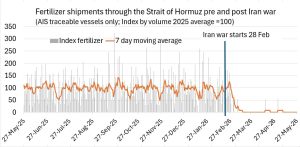

Strait of Hormuz disruptions linked to the Iran war have choked off fertilizer shipments from the Middle East and pushed prices sharply higher, prompting a wave of emergency support and trade measures as governments try to shield farmers ahead of key planting seasons.

We compare and contrast the 2025 financial performance of selected major fertilizer producers.

Yara Australia’s Pilbara facility is expected to remain offline for around two months following a power outage at the site. The incident is understood to have damaged some systems at the facility and that repair work is now required. Initial assessments are indicating a prolonged curtailment of both ammonia and technical ammonium nitrate production.

Egypt’s $873 million green ammonia project in New Damietta has entered the front-end engineering and design (FEED) phase, with pre-FEED studies for the marine jetty and hydrogen plant already completed, Zawya reported 7 April, citing a statement by the Egyptian Petrochemicals Holding Company (ECHEM). The project is being developed by Damietta Green Ammonia (DGA), a joint venture between Norway’s Scatec, ECHEM and Misr Fertilizers Production Company (MOPCO). FEED work on ammonia export facilities is ongoing, while major permits and financing arrangements are still being finalised.

Co-developed by GEA and Yara, the ATMOS process is an advanced heat integration technology for concentrating phosphoric acid.

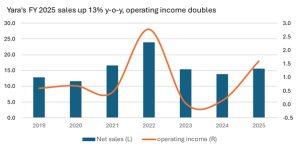

Yara’s full-year earnings (EBITDA) surged to $2.75bn in 2025, driven by stronger nitrogen margins, lower fixed costs and solid volumes.

Air Products and Yara International ASA say that they are working to combine Air Products’ industrial gas capabilities and low-emission hydrogen production with Yara’s ammonia production and distribution network, with several major projects under development.

ATOME has signed a definitive offtake agreement with Yara International for its Villeta project in Paraguay.

From ship to storage, Bruks Siwertell aims to ensure safe, reliable, high-capacity fertilizer transfers.