Nitrogen+Syngas 363 Jan-Feb 2020

31 January 2020

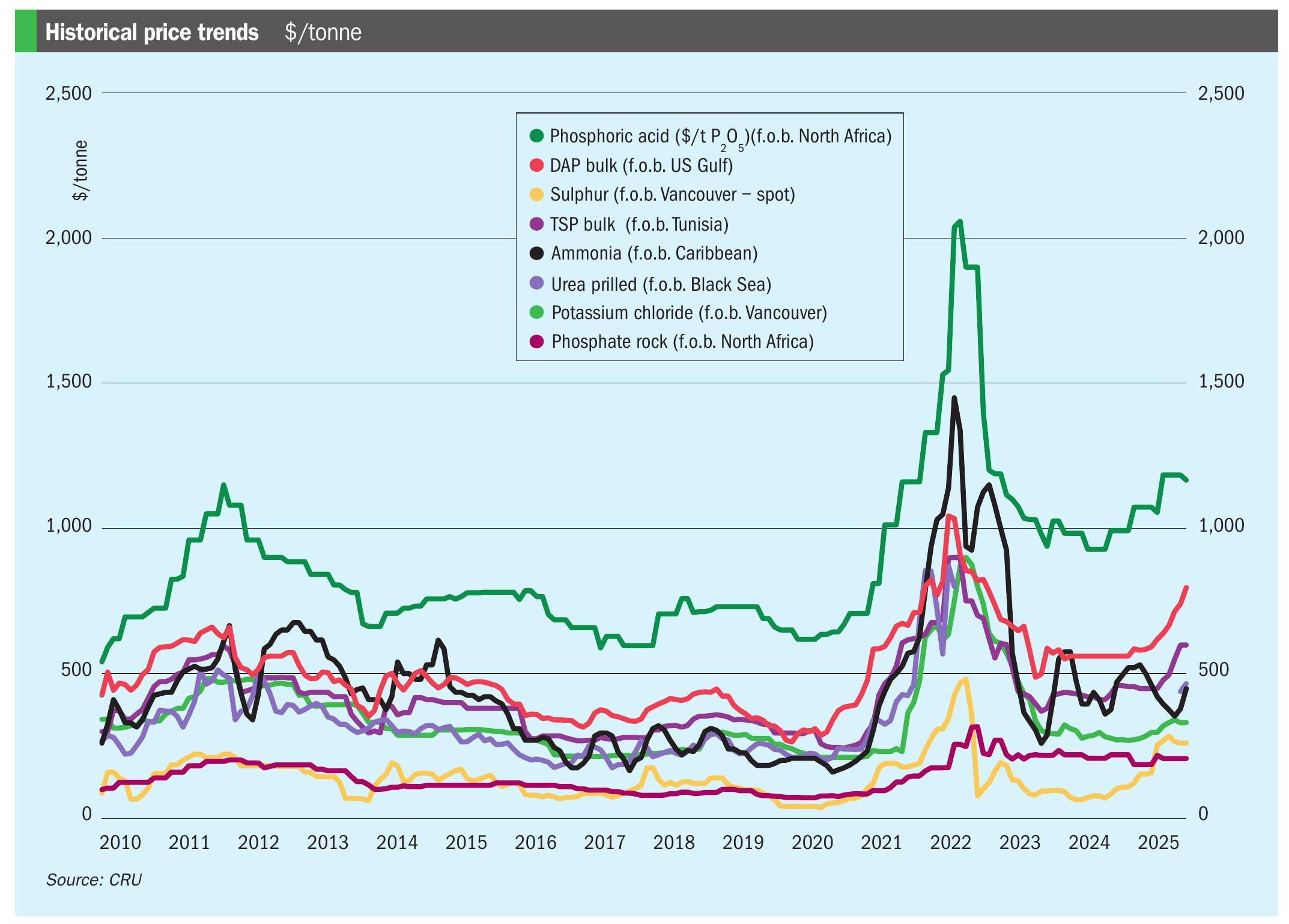

Feedstock pricing and marginal producers

FEEDSTOCK

Feedstock pricing and marginal producers

Floor prices in nitrogen markets are set by marginal producers high on the cost curve, usually using higher cost feedstocks. Recently, lower coal prices in China and the cost of imported LNG have begun to change the dynamic between producers on the margins.

In times of relative oversupply in the urea and other nitrogen markets, prices tend to be set by the production costs of producers at the margins. In the past decade, these have generally been either gas-based producers paying high imported gas prices, such as in Ukraine or India, or domestic, mainly coal-based producers in China, with the latter increasingly coming to set the floor price for urea.

Chinese coal prices

Globally, usage of coal dropped in 2019 compared to 2018, according to International Energy Agency figures. Coal-fired electricity generation capacity fell by 2.5% during the year, as concerns about greenhouse gas emissions and cheap natural gas (and falling renewables prices) drive a move away from coal-fired generation. In Europe coal-based power generation is on its way to being phased out, while in the US cheap shale gas has seen the proportion of electricity generated by coal fall from 57% at the turn of the century to 27% in 2018. US coal demand peaked in the late 2000s and has dropped by half since then. European coal demand peaked in the 1980s and has likewise halved since then. In spite of rapidly rising use in India and southeast Asia, global coal use seems to have plateaued and may be slowly falling.

This has led to coal prices falling globally, and China has been no exception. China remains the mainstay of coal demand, accounting for half of all coal consumption, and low international prices meant that the Chinese market sucked in imports from Australia and Indonesia in 2019 in spite of Chinese government attempts to protect domestic coal production. However, it appears that imports are likely to reduce in 2020 as the Chinese government continues to prioritise the development of large, efficient domestic mining operations.

On the demand side, Chinese coal-based electricity generation struggles with profitability, and at the start of 2020 the government introduced a new electricity pricing mechanism with a base price plus a variable ‘float’ range, up to10% above or 15% below the base price level, replacing a one size fits all benchmark tariff set by the National Development and Reform Commission (NDRC). Industry observers believe that the new price structure will result in lower prices in most of China outside of the large east coast cities, as there is already surplus generation capacity. Coal generation is also steadily losing ground to nuclear and renewable power, which the government guarantees purchase of their output to encourage ‘clean’ electricity generation. Aside from a blip in 2017, Chinese coal demand essentially peaked in 2013 and has been falling slowly since then.

The upshot is that – while coal prices in China peaked in late 2017 and early 2018, over the past two years there has been a growing glut of coal in China, leading to lower prices which have helped sustain Chinese urea producers and encourage Chinese exports of urea.

More efficient production

Another factor affecting Chinese coal-based ammonia-urea production has been a switch in terms of gasification technology. The use of more ‘forgiving’ gasification processes which can run on lower grade, bituminous coal rather than higher grade anthracite has led to a marked increase in productivity, coupled with the fact that the newer plants tend to be larger and gain efficiencies of scale in addition to smaller, older plants. Greater use of automation has also reduced staffing costs.

CRU calculates that there has already been a major swing away from anthracite-based production in China, with the proportion of Chinese urea capacity using anthracite falling from 50% in 2013 to 37% in 2019, at the same time that bituminous-based production has risen from 18% of the total to 33% in 2019, and projected to reach 39-44% in 2021. The ability to use cheaper coal has lowered the overall cost of Chinese urea production, although a number of anthracite based plants still exist at the margins.

LNG prices

Urea capacity based upon imported liquefied natural gas has often been at the highest end of the cost curve. Many Indian urea plants effectively operate on imported LNG as India runs a gas deficit.

The same has also become true of some of China’s gas-based capacity. China is also running a gas deficit as it switches towards more gas-based electricity generation. Demand for gas is increasing by up to 10% year on year (a 14% increase has been estimated for 2019), and in spite of new pipelines from Russia, China is struggling to make up the deficit with imported LNG in spite of increased production from sour gas, tight gas and shale gas. In 2018 China imported 74 bcm of LNG, making it the second largest consumer of LNG in the world after Japan, which switched to LNG-based electricity generation after much of the country’s extensive nuclear generation capacity was idled following the Fukishima accident. China overtook Japan last year to become the largest importer of LNG in the world, and the country’s gas demand is expected to reach 510 bcm by 2030, more than double the figure for 2018.

China has been gradually liberalising gas prices but gas pricing in China can still be relatively opaque. Imported gas is typically pegged to global oil prices while domestic gas depends upon netbacks to production costs. A survey by the International Agency for Energy Economics in 2018 found gas prices ranging from $6-13/MMBtu throughout China, depending on location. However, what is clear is that these prices are high compared to gas prices in other major nitrogen producing countries like the US or Russia, and even India. This puts Chinese gas-based urea capacity towards the top of the cost curve, and as a result gas-based capacity in China has been squeezed, falling from 29% of urea availability in 2013 to 26% in 2019. Feedstock availability has also been an issue, with gas supply restrictions to Chinese gas-based urea producers during the peak winter electricity demand season.

Set against this, LNG prices have fallen as supply grows faster than demand. LNG exports from the US and Australia, amongst others, are set to increase LNG supply by 100 bcm between 2018 and 2023. In spite of rapidly growing Asian demand, particularly from China, and the US-Chinese trade dispute disrupting US deliveries to China, delivered LNG prices to northeast Asia had fallen from $9-10.00/MMBtu in 2018 to $5.10-5.20/MMBtu at the start of January 2020, lower than domestic Chinese gas prices. Delivered LNG prices to Europe were just $4.00/MMBtu.

India

India is developing new urea capacity to try and reduce its import dependency, as described in our article elsewhere in this issue. However, with the exception of the Talcher plant, which will use coal feedstock, all of the new urea capacity will depend on ammonia made from imported natural gas, as India does not have sufficient domestic gas capacity to operate these plants, and imports roughly half of its natural gas needs. Like China, India also often restricts gas availability during peak demand seasons, which coincide with periods of low rainfall when hydroelectricity is less available. The four new gas-based plants, together with the Talcher unit, should take India’s urea capacity from 26.6 million t/a in 2019 to 33 million t/a in 2023.

Since 2014, Indian domestic gas prices have been linked to international gas hub prices such as Henry Hub in the US and the EU-UK International Balance Point. As a result, Indian domestic wholesale gas prices are held artificially low; at the start of January 2020 they averaged around $3.25/ MMBtu. However, Indian urea producers do not pay this price, but rather a composite ‘pooled’ gas price which is also influenced by LNG prices, and the share of domestic gas consumed by the Indian fertilizer industry has shrunk, from around 60% in the 201415 financial year to just 30% in the 201920 financial year. Regasification costs are high in India, and this has pushed the pool price for fertilizer producers to over $10.00/ MMBtu for most of the past two years. This comfortably puts Indian urea plants towards the top of the global cost curve. While LNG prices have fallen for the time being, India’s fertilizer producers will be further exposed to global LNG prices, at the same time that low domestic wholesale prices do not encourage new exploration and production activity, meaning that the import gap will grow. However, as the Indian government has taken a strategic decision to operate urea capacity no matter what, it may pay the subsidy no matter what, and operating rates may not be closely linked to gas prices, at least until the new nutrient based subsidy scheme allows domestic fertilizer prices to float towards a market rate.

China still the floor setter

What does all of this mean for urea prices? Although Indian urea capacity is among the highest cost production worldwide, it is supplying a guaranteed domestic market and remains subsidised. As a result, it is China that continues to set the floor price for urea. The switch away from anthracite towards bituminous coal and the gradual sidelining of gas-based capacity in China means that increasingly it is the production costs of Chinese bituminous-based producers which will come to dominate. In November 2019, CRU put those costs at $275/tonne. One other factor to consider is the ongoing closure of Chinese urea capacity. Although new, larger and more efficient plants continue to be built, economic and environmental related closures have seen 19 million t/a of Chinese urea capacity close since 2013, and another 13 million t/a (net 5 million t/a) is likely to close by 2023. Chinese urea exports have already fallen from a peak of 13.7 million tonnes in 2015 to 2.4 million tonnes in 2018, although last year’s lower coal prices and the falling remnimbi against the dollar encouraged more exports in 2019, and the 3Q 2019 figure had already reached 3.2 million t/a, with the full year figure is likely to be closer to 4.5 million tonnes. Continued capacity closures may reduce China to a seasonal exporter only, with producers elsewhere in the world setting urea prices outside those periods.