Sulphur 387 Mar-Apr 2020

31 March 2020

Uncharted territory

“Russia and Saudi Arabia have chosen this moment to have a price war…”

This year appears to be determined to illustrate the limitations of forecasting. Projecting trend lines into the future, looking at expected completion dates for major projects and global economic projections are all worthwhile activities, and can provide valuable insights for business people, but any prediction is apt to be derailed by what one of our prime ministers supposedly once described airily as; “events, dear boy, events.”

On the phosphate side of the business, the sulphuric acid industry is intimately connected with agriculture via demand for fertilizers, which is always dependent upon the vagaries of weather, and hence suppliers are used to a degree of variability and volatility. However, the events of 2020 look to be quite seismic ones for all industries and their effects are far harder to predict.

This year’s main ‘black swan’ – long predicted in principle but completely unexpected as to timing – is of course the outbreak of the Covid-19 virus, beginning in China’s Hubei province, but at time of writing now spread to all of the continents of the world, and especially virulent in South Korea, Italy and Iran. While China’s draconian quarantine measures seem to have contained the outbreak there for now, the effects of the pandemic are still working themselves out across the world, and predictions range from the mild to the apocalyptic. What is more certain is the chilling effect on the world economy, with the airline and wider travel industries virtually shutting down. Quarantining entire nations, as Italy announced yesterday, are of course vital and life saving measures, but will nevertheless have huge consequences in terms of the associated disruption.

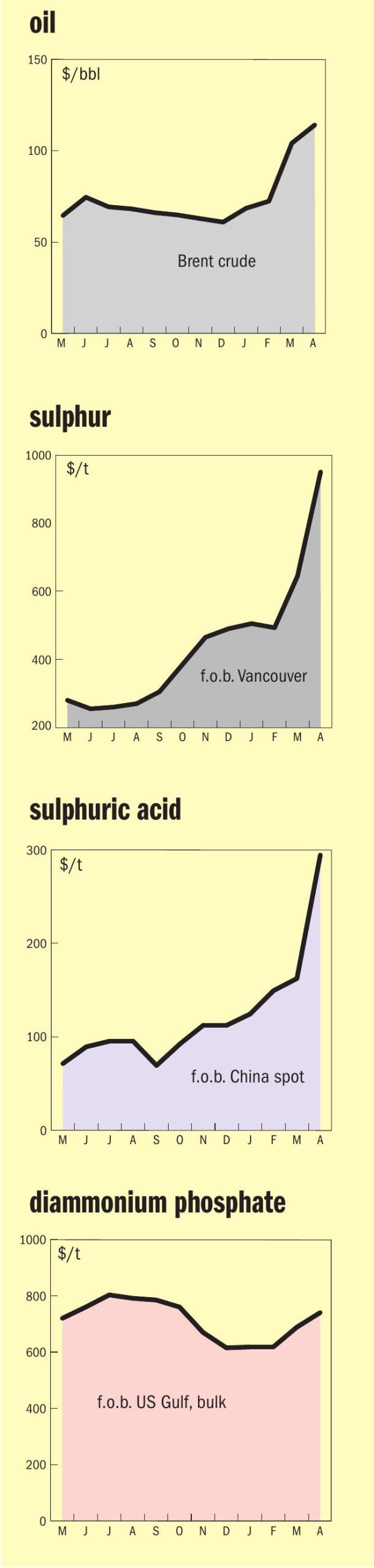

At the same time, Russia and Saudi Arabia have chosen this moment to have a price war in the oil industry. Russia, though not formally part of OPEC, had long cooperated on oil production, but decided in early March to break ranks. The impetus was, perhaps inevitably, Covid-19, or in this case the reduction in global oil demand caused by lockdowns, shuttered factories and cancelled flights – China’s oil imports dropped by 20% in February alone. OPEC had suggested a 1 million bbl/d production cut, with Russia bearing half of that. Russia balked, and Saudi Arabia has opened up the taps as a countermeasure. Both countries appear to be secretly hoping that the real casualty will be the US tight/shale oil industry, heavily indebted and not able to bear a long period of low oil prices. WTI prices fell to $28/bbl this week – lower than during the 2008 price crash, and reaching levels not seen since 2004. But given both Russia’s and especially Saudi Arabia’s dependence on oil revenues, they will also feel the pain of a prolonged period of low prices. A revival in the Chinese economy could still turn this around, but there are some long lean months ahead. The worsening economic gloom has in turn triggered a stock market sell-off that has already been called ‘Black Monday’. Bond yields have gone negative and the prospect of a global recession is looming. How much of this is merely short term panic remains to be seen.

For the sulphur industry, smaller refinery runs means less supply, but the question will be how the demand side holds up, and that means industry and agriculture. On the acid side of the equation, Chinese lead, zinc and copper mines have reduced output, but smelters have continued operating, and quickly run out of acid storage capacity, forcing shutdowns among smelters as well and sending acid prices into negative territory. The main demand centre – China’s Hubei province, which produces 30% of the country’s phosphate fertilizer – has been the worst affected by Covid-19. If China has got a grip on the epidemic, and this is a temporary blip, the spring fertilizer application season may rescue the situation, but that remains highly uncertain. In the interim, major consumers like India have been forced to look further afield, to Saudi Arabia, Morocco and the US.

The remainder of the year appears to be shrouded in far greater uncertainty than anyone might have expected just a few short weeks ago. Everyone must now consider any number of factors that they may not have previously given much thought to. Perhaps the only advice under such circumstances are the words of president Dwight D. Eisenhower: that “plans are worthless, but planning is essential.”