Fertilizer International 501 Mar- Apr 2021

31 March 2021

Market Insight

Market Insight

Market Insight courtesy of Argus Media

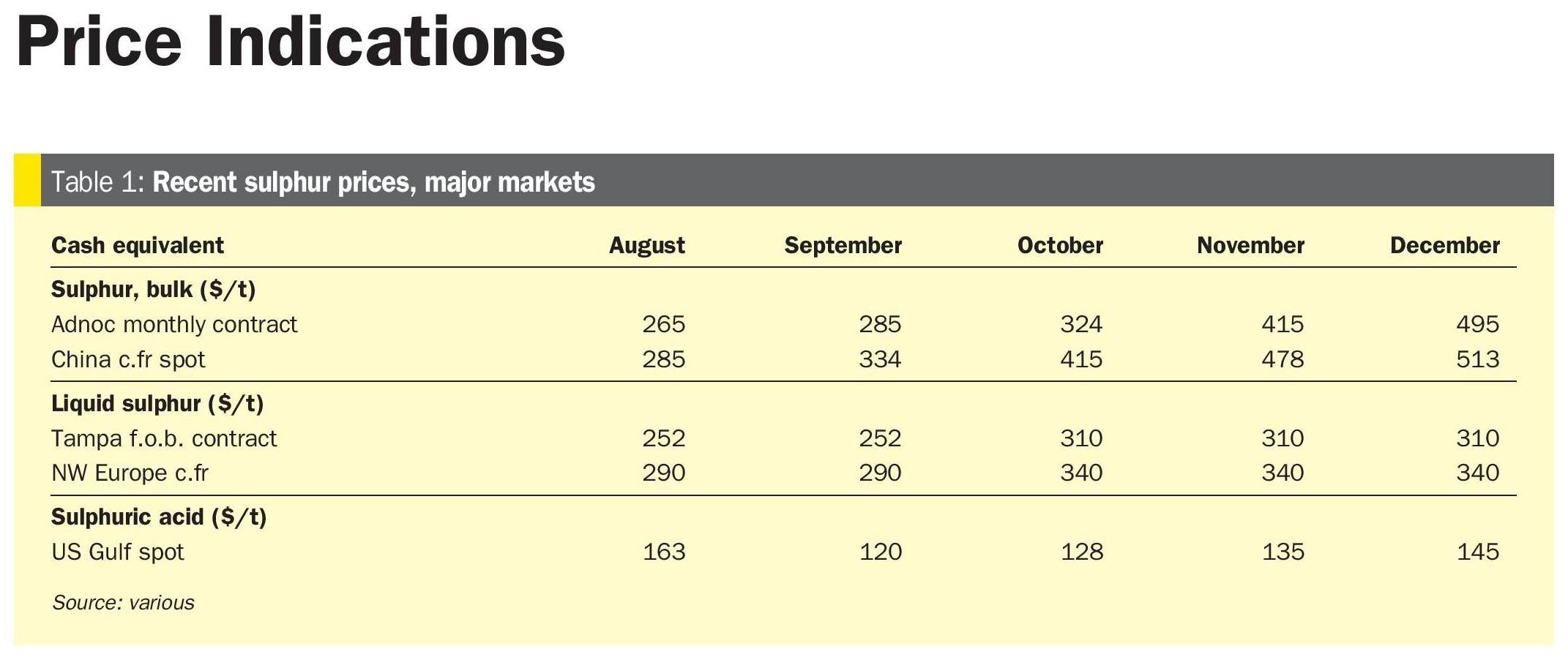

PRICE TRENDS

Urea: The jump in freight rates has been a dominant market topic. Rates have continued to rise since the initial hike in late February, with Middle East-Brazil freight now quoted at $38-40/t, double the rate at the start of the year. New sales of urea have been impeded by the volatility and uncertainty this has created.

Urea prices have moved up in both Egypt and the US while remaining stable elsewhere. Egypt is benefiting from strong demand from Turkey, while the US needs to buy substantial quantities of granular urea for May arrival. Although US production plants are now restarting, after gas-related closures in February, additional imports will still be needed to cover lost output.

Elsewhere, the 2021 demand outlook looks very favourable, with crop plantings, spurred on by attractive grain prices, forecast to rise across the globe.

Key market drivers: agricultural demand, the US and freight.

Ammonia: Another spate of spot market deals were concluded at steep premiums to previous business. This pushed Black Sea f.o.b. prices and US Gulf cfr prices to highs not seen since late-2015.

Severe supply tightness continues to dictate sentiment. Consequently, producers are able to lift offers significantly as spot cargoes become available. The supply deficit is most concentrated around the US, where four production plants remain offline in the US Gulf. A number of plants also remain offline in other regions due to weather-related gas shortages.

Trinidadian producers are ramping up production as much as possible. Nutrien, whose production outage on the island continues, needed to step into the market at the end of February to buy more Algerian tonnes at a price netting forward to $470/t cfr US Gulf. Spot sales are adding upward pressure to the upcoming March Tampa settlement, with a huge increase on February’s $330/t cfr price expected.

Key market drivers: US season concerns, the Ukraine (Pivdenny) price jump (over $40/t) and the Saudi Arabian outage.

Phosphates: US barge prices softened in late February, with MAP standing at $560565/st f.o.b. Nola in the last week of February. This price is equivalent to about $611-617/t cfr – and therefore in-line with Brazilian MAP prices, which Argus assessed at $615-620/t cfr in late February. The change in price direction comes after weeks of hefty US premiums, with supply tightness driving up barge values ahead of spring application. The focus has now shifted to buyers lining up phosphates in Brazil.

Further strong gains were made in China in late February. DAP export prices rose to $530-563/t f.o.b., on business to Southeast Asia and Central America, compared with $515-520/t f.o.b. the previous week. Indian DAP import prices remain flat.

Key market drivers: Indian importers raising the DAP maximum retail price (MRP), Jorf Lasfar loading delays and the softening of US barge prices.

Potash: Standard MOP prices rose in Southeast Asia, after fourth-quarter volumes sold into the local market dried up. Brazilian prices also continue to rise on supply constraints and high demand. SOP prices, meanwhile, remain steady in Europe, despite rising costs for Mannheim producers, although second-quarter negotiations are still to come in many cases. Freight rates for dry bulk vessels continue to rise, mitigating f.o.b. price increases.

Key market drivers: China’s return to the market and pending decisions on contracts from suppliers.

NPKs: Late February f.o.b. prices held steady, for the most part, yet delivered prices continued to tick higher on a rising freight market. Spikes in both container and bulk freight prices have reduced export interest in seaborne trade. Many European producers have sufficient demand from their own domestic or neighbouring markets. Fulfilling this demand via train and trucked deliveries has been more cost-effective than small seaborne shipments. This is amid strong demand for vessels from a range of commodities and rising bunker fuel costs.

Indian import demand strengthened ahead of the forthcoming kharif season. Fact tendered to buy 25,000 tonnes of NPS (2020-0+13S) for mid-April delivery, and separately tendered for 25,000 tonnes of NPK (16-16-16) for mid-May delivery. At least four Indian producers have planned maintenance across six NPK/NPS plants in March-April, temporarily curbing domestic output.

In Africa, One Acre Fund tendered for almost 7,000 tonnes of NPK (17-17-17), as well as DAP and urea for the Rwandan market, for delivery via Dar Es Salaam or Mombasa by 15 April.

Key market drivers: End of spring season in Eastern Europe and the forecast rise in global grain output.

Sulphur: Buyer resistance to the steep increments in recent f.o.b. sales is increasing and limiting deals. As a consequence, sulphur f.o.b. price levels are now out of touch with cfr pricing in some markets. To date, the limited supply situation has enabled suppliers to increase prices, despite firming freight costs. But resistance is increasing and most markets have yet to accept the above cfr price levels of latest offers ($215-220/t). The difficulty in booking vessels is also starting to have an impact. Despite buyer demand, product lifting may be a challenge if vessel availability remains very limited. The imminent announcement of March lifting prices is, however, expected to release some cargo to the market.

Key market drivers: rapidly firming f.o.b. prices coupled to greater buyer resistance to this.

OUTLOOK

Urea: Although price stability prevails in many areas, some marginal gains in f.o.b. levels are likely in March, possibly affecting North Africa and the US. The urea market is forecast to swing to a surplus in the second-quarter as demand wanes in the west and new capacity comes on-stream.

Ammonia: Some producers are already reporting to be sold out for April. Price increases into May are therefore widely expected. The trade balance is forecast to move into surplus in the second-quarter, prompting gradual price falls from April as production normalises.

Phosphate: Supply tightness is expected to persist into the second-quarter. Following recent sharp phosphates price rises, levels should remain firm through the first half of the second-quarter. The scarcity of duty-free MAP for the US market has supported prices across the globe. East of Suez, surging demand from regional Asian markets has pushed price levels higher, with Chinese producers continuing to focus on their domestic market. Anticipation of an Indian subsidy rise could act to support fertilizer buying on the subcontinent.

Phosphate: MOP price rises are set to continue, spurred on by the shortage in granular product availability and higher demand compared to this time last year. SOP prices are also expected to increase, especially from Mannheim producers, if only to cover rising feedstock and freight costs.

NPKs: Very limited spot supply and raw material prices rises are exerting an upward pressure on NPK fertilizer prices, despite the pause in the market.

Sulphur: Although pricing continues to experience upward pressure, the steep level of recent firming is not expected to be sustainable. The likely breaking point will happen when phosphate pricing begins to slacken, and/or when the sulphur supply situation eases, whichever occurs first. The market is then expected to undergo a potentially fairly swift price correction to the preceding rapid rise.