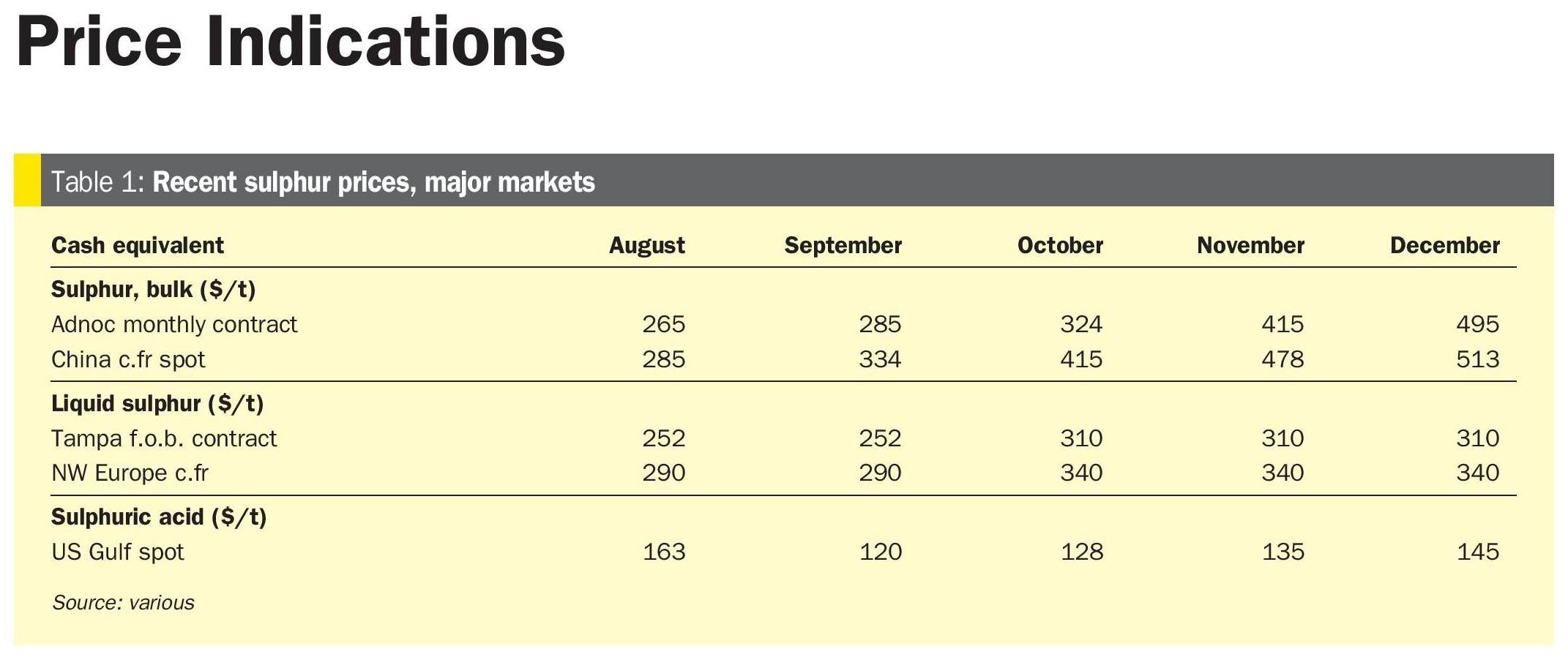

Fertilizer International 507 Mar-Apr 2022

31 March 2022

Brazil’s fertilizer market

LATIN AMERICA FOCUS

Brazil’s fertilizer market

Debora Simoes, Bruno Fardim, and Cleber Vieira of Agroconsult report on what’s driving the Brazilian fertilizer market currently and look at prospects for the coming year.

2021 – a remarkable year

2021 proved to be a remarkable year for fertilizer consumption in Brazil. Fertilizer product deliveries reached 45.96 million tonnes, Agroconsult estimates, setting a new record high. To put this in context, this total is 5.4 million tonnes up on 2020 – the previous high – an increase that is equivalent to the entire fertilizer consumption of Argentina, Latin America’s second largest fertilizer market after Brazil.

This was the second year in a row that Brazil’s agricultural sector registered a double-digit growth in fertilizer consumption (Figure 1). This growth was largely driven and sustained by the rapid improvements in farm profitability during the 2020/21 and 2021/22 crop seasons. This, in turn, was due to a combination of the price upsurge for leading agricultural commodities during the Covid-19 pandemic and the falling exchange rate of Brazil’s currency (Brazilian Real, BRL) versus US Dollar.

The extremely high soybean profits in Mato Grosso state, one of the Brazil’s main agricultural regions, in 2020/21 and 2021/22 provide a good example (Figure 2). Average profits in the latest 2021/22 crop year have tripled from their 2019/20 pre-pandemic level.

Higher earnings in 2020/21, together with positive prospects for the coming season, enabled Brazil’s farmers to pre-buy their 2021/22 crop season fertilizers in late 2020 and at the start of 2021, using additional cash to take advantage of the more favourable barter ratio, i.e. the amount of harvested crop necessary to buy one tonne of fertilizer (Figure 3).

By December 2020, about 40 percent of the fertilizers for delivery and use in 2021 had already been purchased in advance, according to Agroconsult’s periodic survey with sales representatives. This advance purchase rate by farmers would typically be below 10 percent in normal years.

Imports at a record high

On the supply side, the Brazilian fertilizer market remains highly import-dependent. This makes logistics a critical factor in ensuring fertilizers are delivered to farmers on time and at a competitive cost. Overall fertilizer imports reached a record high of 39.15 million tonnes in 2021, equivalent to some 83 percent of fertilizer supply. Fertilizer imports through Brazilian ports rose by 6.3 million tonnes year-on-year in 2021 – creating operational challenges across the whole value-chain. Consequently, Brazil faced issues in distributing these imports to meet the exceptional demand levels seen in 2021. Unloading delays in ports (Figure 4), late deliveries to farms, and even shortages of specific types of NPK, were some of the common complaints reported to us last year.

Prospects for 2022

In the current geopolitical situation, forecasting is a tough task for even the most experienced analyst. At the time of writing (end of February 2022), in the immediate aftermath of Russia’s invasion of Ukraine, prospects for 2022 fertilizer deliveries to Brazil remain positive.

Agroconsult is forecasting that Brazilian demand may reach 46.53 million tonnes in 2022 – up 1.2 percent on 2021 and a year-on-year increase of 574,000 tonnes. With average fertilizer application rates expected to remain flat, this growth in fertilizer use is expected to be largely driven by a 1.7 million hectare expansion in the crop planting area (Table 1).

While farm incomes for 2022/23 still look positive – and above the five-year average – they are expected to fall by about 40 percent on the previous crop season. One reason for this is the acrossthe-board increases in agricultural input prices, particularly for fertilizers, now facing Brazil’s farmers as they plan for the 2022/23 crop season. For example, the planting costs for a hectare of soybean in 2022 look set to be 27 percent higher than last year (Figure 5).

The severe drought in the south of Brazil has also been affecting farmers and the agricultural market. This region accounts for about one-third of the planted area for soybean and summer corn. Agroconsult estimates that so far this year more than 18.5 million tonnes of grains have been lost due to dry weather conditions. Total losses exceed 40 percent of expected production in some regions. As a result, famers in the most affected regions have registered financial losses after more than 10 years of good profits.

The drought could also hit fertilizer demand. Most summer crops in the worst affected regions, for example, were incapable of extracting much of the applied potassium. It is therefore expected that the remaining residual K still available in the soil will be sufficient to meet the February-June demand of this year’s winter corn crop.

Looking ahead, it is the 2022/23 crop season and the start of planting in September that will determine the size of the fertilizer market this year. At the time of writing, farmers in the south of Brazil have not yet decided if they will reduce their average fertilization rates for 2022/23, as they usually wait until the end of the current harvest season in May-June before making this decision. Currently, Agroconsult still believes that average fertilizer rates in the region – noted for the strong presence of agricultural cooperatives – will be maintained due to credit availability. This is due to the money received from insurance companies as well as the positive financial results obtained in previous years.

Logistics is another important factor to highlight. Delivering 46.5 million tonnes of fertilizer to Brazil’s farmers in 2022 will require a concerted effort by all participants in the fertilizer supply chain. With imports expected to reach 40.0 million tonnes this year, famers, blenders, fertilizer producers, port terminals and logistic companies will all need to work together and plan in advance. This will be necessary to avoid the port unloading delays seen in 2021 and minimise the risk of product shortages.

In fact, it would be an important and great achievement if the share of imported volumes needed to cover demand until September was already domestically available mid-year to build up inventories. This is especially true in 2022, given the challenges of the international market, and the risks surrounding Russian and Belarusian fertilizer supply to the Brazilian market (see box).

Authors’ note

The information in this article was correct at the time of writing (end-February). However, future Brazilian fertilizer supply could be influenced by the deepening conflict in the Ukraine, which has created a fast-moving and volatile market situation.

Russian fertilizer supply to Brazil

At the time of writing, although Russia’s fertilizer sector has not been specifically targeted by the economic sanctions imposed by western countries, the war in Ukraine itself could put Brazilian fertilizer supply at risk by creating logistical obstacles and affecting Belarus and Russia’s ability to export.

Current situation

Russia plays an important role in global fertilizer trade, having a significant market share of international nitrogen, phosphorus and potash exports. Brazil, in particular, is highly dependent on Russian fertilizer supply. Russia and Belarus are strategic fertilizer trading partners with Brazil. Together, they supply about one-third of the country’s total fertilizer imports (Figure 6) – 28 percent for nitrogen, 45 percent for potash and 15 percent for phosphate fertilizers.

While other countries could step in to replace current Russian supply to Brazil, fertilizer producing companies would have to mobilise quickly. As there would be an urgent need to rapidly settle contracts with new partners and reorganise logistics to avoid any subsequent supply problems. Any delays could raise the risks to Brazilian market supply in 2022.

What is the invasion of Ukraine likely to change?

International fertilizer prices are likely to rise again. The risk of a supply crisis is also likely, especially if the conflict affects shipments by creating logistical bottlenecks, or if barriers to Russian fertilizer exports are introduced as part of tougher economic sanctions.

If western countries impose further trade sanctions, Russia could also retaliate by cutting the natural gas exports the west needs for nitrogen fertilizer production, resulting in shutdowns and output cuts in the European Union.

Spring demand in the northern hemisphere (typically 80 percent of global fertilizer consumption) will have been largely met by the end of the year’s first quarter – enabling the 2022/23 crop season there to start with few impediments. Whereas countries in the southern hemisphere, including Brazil, are likely to have to deal with the consequences of the conflict such as higher prices and possible supply shortages.

There is a possibility that barter transactions between fertilizers and grains – which have been improving on the back of higher soybean and corn prices – may become unfavourable to Brazilian farmers. If that were to happen, the likelihood of a drop in Brazil’s fertilization rates for the 2022/23 crop season, and a corresponding downgrade to current market projections for 2022, is a risk that cannot be ignored.