Fertilizer International 521 Jul-Aug 2024

31 July 2024

Pathways to sustainable agriculture

SUSTAINABILITY

Pathways to sustainable agriculture

The production and use of nitrogen fertilizers are responsible for around five percent of global greenhouse gas (GHG) emissions. The fertilizer industry will need to drastically cut these emissions by 2050 as part of its contribution to the 1.5 °C global warming target. Yet around 48 percent of the global population rely on crops grown with nitrogen fertilizers. Guaranteeing food security, by continuing to supply affordable crop nutrients at scale, while transitioning to a low-carbon future, is therefore the collective challenge for the global fertilizer industry and world agriculture.

A decarbonisation trilemma

Mineral fertilizers are vital for world food production and security. By raising crop yields – and so boosting the amount of food produced from a fixed area of agricultural land – they are responsible for feeding around half the global population1 . Yet nitrogen fertilizer use is associated with annual greenhouse gas (GHG) emissions of around 717 million tonnes (Mt) carbon dioxide equivalent (CO2 e) a year2 . This is broadly equivalent to the total emissions of Germany. Furthermore, use emissions from farm land are primarily in the form of nitrous oxide (N2 O) – an ozone-depleting gas with a global warming potential almost 300 times greater than carbon dioxide.

Emissions from nitrogen fertilizer use, when combined with those generated by its production, collectively account for around six percent of total food sector GHG emissions, a sector which itself is responsible for around one-third of total global GHG emissions.

In recent years, fertilizer producers, primarily through the International Fertilizer Association (IFA), have been working collaboratively on plans to reduce their GHG emissions by 2050 and ensure the global fertilizer industry plays its role in meeting the Paris Agreement’s 1.5°C limit on global warming. The challenge for the industry and policymakers is threefold:

- How to place the agricultural sector on a sustainable low emissions trajectory

- While continuing to supply framers with the fertilizers they need to feed an ever growing population.

- Yet do so without imposing a crippling cost burden on fertilizer producers, farmers, the food industry and ultimately food consumers.

Driving down production emissions

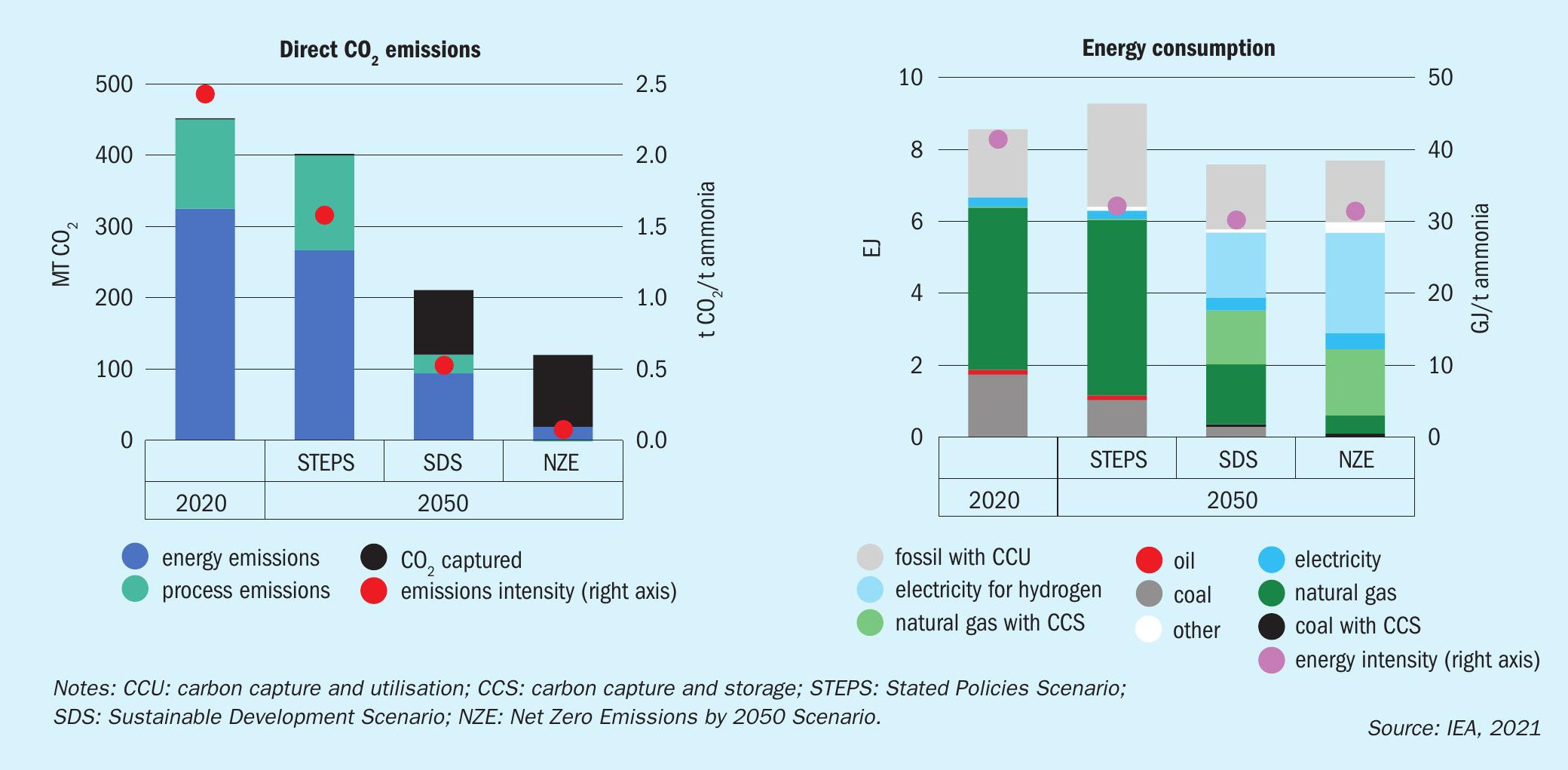

The Ammonia Technology Roadmap – a collaboration between the International Energy Agency (IEA), the European Bank for Reconstruction and Development (EBRD) and IFA – was published in October 2021 just ahead of the COP26 climate conference in Glasgow3 . Described by IFA at the time as its number one priority (Fertilizer International 505, p36), the roadmap set out a plan to decarbonise ammonia production globally by 2050. This report and its findings have been covered in depth previously (Fertilizer International 508, p38).

Producing ammonia requires a lot of energy. On average, around 2.4 tonnes of carbon dioxide are emitted per tonne of ammonia produced, although this varies according to the hydrocarbon feedstock used. To put this in context, ammonia’s per tonne emissions intensity is twice as high as steel, for example, and four times higher than cement.

Direct emissions from global ammonia production currently total 450 Mt CO2 e per annually. This is comparable to the total emissions of South Africa.

The IEA/IFA roadmap sets out three future scenarios for ammonia production out to 2050 each with a different set of actions and outcomes (see box). Two scenarios – SDS and NZE – achieve 70-95 percent emissions reductions by 2050. These deep emissions cuts will be hugely costly. Indeed, meeting or going beyond Paris Agreement climate goals will require the global ammonia industry to invest $14-15 billion in production decarbonisation annually, according to IEA estimates.

The deployment of low-carbon technologies is expected to do most of the heavy lifting on emissions reductions out to 2050. In the SDS scenario, for example, ammonia production via electrolysis powered using renewable electricity would account for around one-fifth of global production by 2050 (versus less than 0.01% today), this share rising to above 40 percent in Europe, India and China. In the NZE scenario, meanwhile, the global production share for the electrolysis pathway doubles to more than 40 percent.

Carbon capture and storage (CCS) also looks set to play an increasing role, capturing 91 million tonnes and 101 million tonnes of ammonia industry CO2 emissions annually by 2050 in the SDS and NZE scenarios, respectively.

These two low-carbon technologies would need to be “deployed at a rapid clip” according to the IEA3 . This is, if anything, an understatement. Under the SDS scenario, for example, more than 110 GW of electrolyser capacity and 90 million t/a of CO2 transport and storage infrastructure would be needed by 2050. That equates to the installation of ten 30MW electrolysers (the largest capacity currently in operation) per month on average, together with the completion of one large-scale CCS project (1 million t/a CO2 capacity) every four months between now and 2050. Even more rapid deployment of these technologies would be necessary under the most ambitious NZE scenario.

“Emissions from the production and use of nitrogen fertilizers are responsible for approximately five percent of the global total – a share that is similar to that of the iron and steel industry, the largest global source of industrial emissions.

Working with the World Business Council on Sustainable Development (WBCSD) and others, IFA is using the ammonia decarbonisation roadmap as a springboard to develop a Sectoral Decarbonization Approach (SDA) for the fertilizer industry to drive down Scope 1 and 2 emissions as part of the Science Based Targets initiative (SBTi)2 .

Action plan on fertilizer use emissions

For the fertilizer industry – and its agricultural and food industry partners and customers – meeting Paris Agreement climate goals is not just about delivering a 70-95 percent cut in the 450 Mt CO2 e of direct emissions currently generated by ammonia production globally. It also means tackling the even bigger 717 Mt CO2 e annual emissions associated with the global use of nitrogen fertilizers by farmers – so-called Scope 3 emissions.

IFA again has addressed this head on by commissioning a comprehensive report and action plan on Scope 3 emissions from UK-based change consultancy Systemiq. Published in September 2022, this report sets out a pathway for reducing global GHG emissions from nitrogen fertilizer use by 70 percent by 2050 – while feeding a global population of 10 billion2 .

This drastic reduction in fertilizer use emissions could be achieved by applying existing knowledge and technologies, according to Systemiq. The report’s findings – and its pathway to a more sustainable agricultural system –are summarised in Figure 2.

Overall, there is potential to cut Scope 3 nitrogen fertilizer emissions from global farming by 69-72 percent (from a 2020 baseline), suggest Systemiq, by applying the following emissions reduction measures sequentially:

- Improved nutrient use efficiency (NUE): potential to reduce use emissions by between 220-415 Mt CO2 e. NUE is increased to 65–75 percent through adoption of best practices by farmers. These include the existing 4Rs framework on nutrient stewardship: applying the right nutrient source, at the right rate and time and in the right place.

- Greater use of nitrification and urease inhibitors: potential to reduce use emissions by 135-235 Mt CO2 e. Inhibitors are applied to half the crop area and half the area fertilized with urea, respectively. This reduces direct nitrous oxide emissions on those areas by 30–50 percent and the fraction of nitrogen from urea that is lost to volatilisation by 30–60 percent. The report also envisages greater adoption of controlled-release fertilizers (CRFs) and other types of enhanced efficiency fertilizers (EEFs) in future.

- More legumes in crop rotation: potential to reduce use emissions by 25 Mt CO2 e. The share of legumes in crop rotations is increased from around 14 percent to 20 percent of global cropland. Growing more legumes such as soybeans can reduce nitrogen fertilizer use – and therefore the associated agricultural emissions – as they can fix nitrogen directly from the atmosphere.

- Land sparing: potential to reduce use emissions by 50-65 Mt CO2 e. This is achieved by a dietary shift away from animal products that allows the release of agricultural land away from crop production.

Additionally, there is potential to neutralise the remaining 30 percent of use emissions (205-225 Mt CO2 e), according to Systemiq, by supporting soil carbon sequestration. This improves soil health while providing a source of income for farmers through carbon farming (Fertilizer International 509, p32).

Systemiq’s report does make a number of underlying assumptions about ag productivity growth. With no productivity growth, use emissions from nitrogen fertilizers would be expected to increase by a further 180 Mt CO2 e by 2050. Systemiq scales this increase back to around 35-110 Mt CO2 e by creating a more realistic ‘business-as-usual’ scenario for 2050. This assumes the global population grows in line with UN projections, agricultural productivity growth of 0.8–1.1 percent per annum (p.a.) and nitrogen uptake growth of 0.4–0.6 percent p.a. Additionally, it is assumed that the gap in nitrogen application rates between Africa and the current global average closes by between one-and two-thirds.

Regional approach

The IFA/Systemiq report identifies measures that could deliver 84 Mt CO2 e of emissions savings globally across six regional cropping systems. Around one-quarter of the emissions reduction measures identified generated a cost saving for farmers – as more efficient fertilizer use should reduce crop inputs while maintaining or improving crop yields.

The savings opportunities primarily come from the adoption of best fertilization practices and changes to crop rotations. While many measures deliver cost savings, farmers still face barriers to change such as:

- Credit constraints and other financial market failures

- Perverse public policy incentives

- Lack of knowledge or access to appropriate skilled labour

- Lack of scale to enable technology adoption.

Major emissions savings opportunities were identified in two regional cropping systems in particular:

- Maize-soybean in Brazil. Raising NUE to 70 percent across Brazil: potential 21 Mt CO2 e emissions savings, although use of precision agriculture by farmers faces cost and staffing barriers.

– Adding inhibitors to sugarcane fertilized with nitrogen and vinasse: this is a low cost measure with potential emissions savings of 2.7-8.1 Mt CO2 e, although there are no strong incentives for farmers to change their behaviour. Insert soybeans into fallow period of the sugarcane crop cycle: highly profitable option for farmers, given high yield and low production costs, but delivers only limited emissions savings of around 0.2 Mt CO2 e.

- Wheat-maize in North China Plain. Adoption of precision agriculture at an annual investment of e2-5 billion: potential 11.2 Mt CO2 e emissions saving. Diversifying crop rotation with legumes: potential 8.7 Mt CO2 e emissions saving, although crop yields would need to rise above the 3 t/ha global average for growers to break even.

“Approximately two-thirds of fertilizer emissions take place after their deployment in croplands. Increasing nitrogen-use efficiency is therefore the single most effective strategy to reduce emissions.”

Total life cycle approach

The total life cycle GHG emissions from nitrogen fertilizers were mapped in a 2023 Nature Food paper by Yunhu Gao and André Cabrera Serrenho of Cambridge University’s engineering department4 . The two authors also determined the maximum mitigation potential of various interventions across the whole life cycle. They concluded that total global GHG emissions from the production and use of nitrogen fertilizers could be cut to just one-fifth of current levels by 2050.

They estimated that GHG emissions from the production and use of nitrogen fertilizers (1.31 Gt CO2 e p.a.) are responsible for approximately five percent of the global total – a share that is similar to that of the iron and steel industry (7%), the largest global source of industrial emissions, and cement (6%) and plastics (4%) manufacturing.

They also note that fertilizers use is so ubiquitous that around 48 percent of the global population are fed with crops grown with synthetic nitrogen1 . This made “reducing GHG emissions associated with nitrogen fertilizers an essential contribution to meeting the 1.5 °C global warming target, while also ensuring food security”, in their view.

From a 2050 baseline for life cycle emissions from nitrogen fertilizers (1,664 Mt CO2 e), the study calculates the maximum mitigation potential of five individual interventions by 2050, if applied in isolation (Figure 3):

- Water electrolysis powered by renewables: 450 Mt CO2 e reduction to 1,214 Mt CO2 e

- Electrification of production: 352 Mt CO2 e reduction to 1,312 Mt CO2 e

- Carbon capture & storage (CCS): 417 Mt CO2 e reduction to 1,247 Mt CO2 e

- Demand reduction (improved nutrient use efficiency): 805 Mt CO2 e reduction to 859 Mt CO2 e

- Nitrification inhibitors: 488 Mt CO2 e reduction to 1,176 Mt CO2 e.

They also plotted the GHG emissions trajectory for nitrogen fertilizers out to 2050 for a combination of mitigation options – including the use of water electrolysis for ammonia production, the deployment of nitrification inhibitors and improving nitrogen-use efficiency to reduce fertilizer demand (Figure 4). The resulting combined mitigation potential suggests that total 2050 GHG emissions could be reduced by up to 78 percent to 357 Mt CO2 e.

“We found that approximately two-thirds of fertilizer emissions take place after their deployment in croplands,” say the authors, adding: “Increasing nitrogen-use efficiency is the single most effective strategy to reduce emissions.”

This strategy includes micro irrigation, sowing crops that are able to use nitrogen fertilizers more efficiently due to improved plant breeding, and 4Rs nutrient stewardship – applying the right fertilizers at the right rate and time in the right place.

“[While] changing from steam methane reforming to water electrolysis powered with renewables results in a substantial reduction in production emissions. This alone can reduce 75 percent of production emissions by 2050 but only 27 percent of total emissions, owing to the much larger weight of use-phase emissions,” the authors conclude.

Next steps

The 2022 Systemiq report2 urged the fertilizer industry to reflect on its proposals and use these to help set individual company and sector-wide targets. It also called the industry’s move to a Sectoral Decarbonization Approach (SDA) “an even bigger step, covering Scope 1, 2 and 3 emissions” because this combines Scope 3 emissions guidance with target setting developed by the Science Based Targets initiative (SBTi)

Systemiq also urged governments to take “action to review and refocus food, farming and fertilizer subsidies and to support collaboration across the food and farming sectors to address emissions”2 .

Finally, a focus on product innovation, with greater investment in research and development, was also needed to set the fertilizer industry and agriculture on a more sustainable pathway, suggested Systemiq2 :

“Developing and applying existing technologies and producing new ones. Additional products such as urease and nitrification inhibitors and controlled-release fertilizers have the potential to further help reduce emissions. More research and product development are needed to make these technologies more affordable, and to better understand how they work together and their wider environment impacts.”

References

Decarbonising production – three possible futures

The IEA’s Ammonia Technology Roadmap sets out three future scenarios for ammonia production – each with different sets of actions and outcomes by 2050 (see Figure 1)

- Stated Policies Scenario (STEPS). The industry follows current trends and, while making incremental improvements, falls well short of a sustainable trajectory.

- Sustainable Development Scenario (SDS). The sector adopts the technologies and policies required to put it on a pathway to meet Paris Agreement goals.

- Net Zero Emissions by 2050 Scenario (NZE). A trajectory for the ammonia industry that reaches net zero global emissions by 2050.

While the STEPS scenario is a modest improvement on businessas-usual that only delivers marginal emissions cuts, both the SDS and NZE scenarios deliver desirable outcomes, according to the IEA, by achieving 70-95 percent emissions reductions. These two scenarios would, however, require the ammonia industry to either meet or go beyond Paris Agreement goals.

Stated Policies Scenario (STEPS)

This assumes that progress over the next 30 years is driven by currently stated government policies. This projection is based on current trends in consumption and production and commitments made at the COP26 meeting in Glasgow. In this scenario:

- Ammonia production would increase by 37 percent by 2050, driven primarily by economic needs and population growth

- While emissions from production fall by about 10 percent

- Cumulative direct emissions from ammonia production between now and 2100 would amount to around 28 gigatonnes (Gt)

- This amount is equivalent to six percent of the emissions budget needed to limit global warming to 1.5°C.

The report assumes that actions under STEPS – because they do not improve enough on business-as-usual – are inadequate and would result in unsustainable outcomes.

Sustainable Development Scenario (SDS)

This assumes that governments and industry actions meet the goals of the Paris Agreement and limit the global temperature rise to well below 2°C. The two key elements in this scenario are:

- Cutting direct CO2 emissions from ammonia production by more than 70 percent, relative to today

- Action on nitrogen use efficiency (NUE) to limit the growth in ammonia production and consumption to 23 percent by 2050. Four main actions would make the following individual contributions to this 70 percent reduction in emissions:

- 45 percent achieved by deploying low-carbon technologies – including electrolytic hydrogen generation (30% of emissions reduction) and carbon capture and storage (CCS, 15%)

- Energy efficiency from the adoption of best available techniques (BATs) and operational improvements contributes 25 percent

- Fuel switching – from coal-based production to less energy intensive gas-based production – is responsible for 10 percent of the reduction

This ambitious scenario requires:

- $14 billion in annual capital investment for ammonia production to 2050

- The installation of more than 110 gigawatts (GW) of electrolyser capacity l 90 million t/a of CCS CO2 storage capacity.

Net Zero Emissions by 2050 Scenario (NZE)

This sets out a trajectory for a fall in ammonia industry emissions of 95 percent by 2050. The additional emission reductions in this scenario – compared to the ambitious SDS trajectory – are achieved by even more rapid deployment of electrolysis and CCS technologies. The main difference between NZE and the SDS scenarios is therefore one of degree. Indeed, the NZE Scenario requires only slightly higher annual investment: $15 billion per year to 2050.